By Christian Takushi MA UZH, Switzerland, 17 Sept 2016, released to public on 19 Oct 2016.

Introduction: Three countries should be on our radar this Q4: The USA, Germany and Turkey. Although no major event is due in Germany, global events are influencing the political process there in a way we haven’t seen since WW2. This goes beyond its engine role for the EU. Since our research shows that Germany is the geostrategic ally of choice for most Emerging Powers, especially Russia and China, we’ll look at underreported aspects of the German Political Process. Events in Italy and France over the next few months will also weigh on Germany over the next 12 months. The liberal forces behind “globalisation” and power concentration are facing popular opposition for the 1st time in four decades.

The past few weeks have been busy in politics and financial markets. Some independent analysts say central banks, big banks and financial media are trying to “bring down” the price of Gold and the British Pound ahead of the US elections. But even if that were true, it is important not to miss the bigger or undercurrent developments that are likely to impact the World Economy and the Political Realm in years to come. In my strategic analysis the interconnection (and overlap) between the USA, Britain, Turkey and Germany is at the core of what is driving much of Foreign, Economic and Military Policies these days. With Russia being rather the (outsmarted) victim, and China being economically overwhelmed, but benefitting the most from all the chaos and lack of leadership. We will uncover historical facts that Western analysts pay little attention to. Highly important anniversaries (religiously and geopolitically) are coming for Turkey in 2017 and 2023. This explains to some extent why Turkey is under such pressure & rush to rise as a Power between West and Orient.

In 2016, it is not about who becomes US President, it is about the US Supreme Court and “what” is driving voters across the West: Whether Trump or Clinton wins, the US President doesn’t have the last word in the USA. It can be effectively vetoed. Much more important than Trump or Clinton is the US Supreme Court. These elections are about the shape of the Supreme Court for the next 20 to 30 years. Those judges are there for life; that is why Democrats and Republicans are eager or rather desperate to win these elections. Many judges will have to be replaced soon. Clinton wants to shift the Supreme Court into a liberal camp, while the Republicans want to preserve the long tradition of a once Conservative Supreme Court. So much is at stake, political leaders, banks, business leaders, academia, media and TV channels are all involved in the greatest propaganda war since World War Two. We don’t know who will win yet, but we know already the name of the biggest casualty: the truth.

About an economist’s approach to Political and Geopolitical Research: At the core of our methodologies is the practical assumption that “all nations and agents advance their interests with all means at their disposal”. It is from that vantage point that our Western-Oriental approach can sometimes deliver a different analysis relative to consensus or mainstream media. Our approach encompasses Western ways of thinking and Oriental ways of thinking to analyse a single development. Where Europeans see lines and trends, Oriental people see circles and cycles. The former are driven by “ratio” among other things, the latter by “honour” among other things. The former seek and trust in treaties, the latter take advantage of the former’s naive trust in treaties. Those believing everything is relative, think Moslems are embracing radical Islam out of poverty or lack of opportunity; Oriental people understand most of them are driven by absolute beliefs and duty. No approach is perfect, mine simply seeks to add value with a different perspective.

BREXIT Aftermath weighs on crucial Q4 2016 for America and Europe

The world is bracing for an unprecedented confluence of events and decisions. Among them: US elections on Nov 8th could put an end to Globalisation & Global Trade as we know them; Austria will hold Presidential Elections on Dec 4th possibly leading to an anti-EU victory. Another decision: the EU may have to concede Schengen Visa to Turkey. To complicate matters the US FED is likely to raise Interest Rates and may use the opportunity to exit the tight & dysfunctional bond with the markets it maneuvered itself into since 2008.

BREXIT is weighing on all these developments and we’ll focus on key aspects that consensus is underestimating, but could impact the Economy & Financial Markets. The new British government is already clearly going against some of the key foundational policies that characterised the Liberal World Order since the mid 1970’s. There is open outrage at Mrs. Theresa May, but most global institutions and Western leaders agree that if they act together they can punish Britain hard enough to prevent any other nation to follow suit. It is not about fighting those who want to exit the EU, it is about exiting the (ultra) Liberal Economic Political System we have in place for over 4 decades.

I. BREXIT triggers Rearmament in Europe (U-turn)

While the media is busy speculating on how & when the UK will start the EXIT process and the war in Syria despite lack of progress, it is overlooking the real action: BREXIT is already impacting the Geopolitical Balance in Military & Security. In fact, soon after the BREXIT Referendum became imminent, Berlin began to prepare for a sweeping rearmament. But despite this, the EU is 5 to 13 years behind Britain.

No European nation understood as well as Britain that the world was becoming more dangerous and total reliance on the USA was too risky. Strategic work initiated in 1997 saw the need for Aircraft Super Carriers and in 2001 the UK committed to America’s USD 1 Trillion Joint Striker Fighter Program. In 2017 the breathtaking HMS Queen Elizabeth Aircraft Carrier will be finished. 18 months later the Prince of Wales Aircraft Carrier will join. 25 days after BREXIT the UK Parliament approved the renewal of the Ballistic Nuclear-Armed Submarine Fleet. Britain is the only reliable major US ally in Europe that can project power and defend the USA if under attack.

For two decades most European states dismantled their Strategic Armed Forces, banking on the Policy Mix the West had applied since the mid 1970’s (Mass Immigration, Liberal Free Trade, Wage Competitiveness and Paper Money Stimulus), and that the boom in trade would make wars obsolete. The rise of huge multinationals should in turn accelerate supranational integration. This well meaning but undemocratic attitude has shaped three generations of U.S. and European administrations.

BREXIT has not only jolted the EU Integration Process, it has weakened and possibly shattered the globalization & power concentration push of the political elites and the United Nations. That is why BREXIT was so dreaded.

After Cameron’s unexpected re-election in May 2015 and his commitment to hold a Referendum, Germany began to face the unthinkable: the need to rebuild the Bundeswehr. While Berlin speaks of USD 147 Billion, I expect it to surpass 220 Billion. Germany is late and it knows it will take it 10 years. Soon after the news of Germany’s rearmament, France and other European nations began their own security & geopolitical reviews. What if a rearmed Germany leaves the EU?

Markets utterly underestimated the UK’s geopolitical importance for the EU and the security balance within it. Without the UK, the EU will become a geopolitical dwarf for at least 7 years.

With growing threats to the Global Supply Chain, a network of strategic military bases is crucial. The superbly located UK bases along Britain’s military foresight, history & investment explain why the USA sees it as its closest Military Ally. But this accelerated military spending by Britain and Germany post Brexit is ushering a rearmament across Europe. The impact on the industrial complex, materials, demand for engineers, technicians & soldiers, unemployment, aggregate income & taxes could be significant. Big Picture: Europe is merely the last continent to join the Global Arms Race.

Our estimate is that the real amount to be invested in rearming Germany will be roughly 50% higher than that officially acknowledged. France is responding and so is Poland. France has already offered Argentina to rebuild ist Air Force with long range fighter jets, capable of reaching the Falklands Islands. Thus, post-Brexit France is eager to challenge or at least contain Britain’s military influence at strategic points for global trade and ist back-up routes

The waves of terror attacks over the past 18 months have led to a more security minded Europe. And one of the results of this shift is that political leaders now see popular support to increase spending in Military-Security complexes. This will support manufacturing output.

This acute security situation and the lack of Britain’s support for Berlin’s Fiscal Discipline will allow EU member states to put Austerity Policies aside and to spend again. Budget discipline means little if people don’t feel safe. But safety will sadly be “wishful thinking”. Europe’s change of mind has come too late. While Europe rearms, emerging powers and terror groups are not standing still.

To mention just one factor: The destabilization of the Middle East has passed the point of no return. Western interventionist policies such as Nation Building and Regime Change spearheaded by Washington, Paris and London – flanked by the U.N. – turned out to be total disasters that will dramatically affect Europe’s security in years to come. I still remember the day in 2011 when I irritated a large group of investment professionals that were loudly celebrating the fall of a regime. I said “we shouldn’t be taking out regimes in Arab countries, what will fill the vacuum could be far worse”. Having embraced the official Western narrative, they looked at me in total disbelief.

The world is busy talking about Brexit, Syria and US Elections, but they are omitting the Arms Race to secure or threaten the Transport Routes on which world trade so much depends. BREXIT has only accelerated this process. And the EU has lost the superb network of British Military Bases. The EU loves to invoke NATO, but a growing number of high ranking officers and members of Congress in the USA believe NATO is flawed. The EU has been on an aggressive territorial expansion, with dismantled armies, but relying on the USA for its defence. Officially the USA supportive, because Obama has removed any general that disagreed with him, but the voices of dissent are growing.

Europe’s errors continue to pile up: Panicking about ISIS, Western states portrayed it as the sole “enemy” of the West in order to embrace and equip all sorts of other terror militias and Islamic groups. Many of them have since joined ISIS or run away with the weapons. The geopolitical message we sent to Arab nations has laid the ground for the next two wars in the Middle East: “Arab Sunni regimes = not OK, destroy; Shiite Iranian regime = OK, our new partner”.

The Big Picture: Europe’s rearmament and security awareness has come too late. The secular security deterioration of the continent can no longer be reversed. Within the next 7 years Iranian and Saudi ballistic missiles, most likely armed with weapons of mass destruction, will be able to reach most of Western Europe. Europe may pay a high price for its lack of geopolitical foresight.

II. Berlin in denial – Germany is rocked by the fast Rise of an anti-EU Party

The anti-immigration & anti-EU Party Alternative für Deutschland (AfD) overtook the CDU in Merkel’s home State as 2nd strongest party. Although the North-Eastern State of Mecklenburg-Vorpommern is thinly populated, it marks the 9th time the AfD is able to enter a State Parliament. The trend is up. Experts are at a loss: merely founded 3 years ago, the AfD has achieved big victories. This, despite concerted media campaigns against the AfD and its leader Mrs. Frauke Petry. The AfD is shuttering the extraordinary stability of the German party landscape since WW2. Over the last year, AfD was the 2nd or 3rd largest party wherever state elections where held. Nevertheless, the established parties refuse to talk to the AfD and treat it as a right-wing phenomenon, and overlooking the countless centrist conservative voters that are backing it. Berlin and media try hard to portray AfD supporters as skinheads, neo-nazis and violent elements. But, most interestingly many AfD supporters indicate they would support also the CSU of Mr. Horst Seehofer (Bavarian sister party of Merkel’s CDU) if it would run nation-wide. This hints at the growing common ground between these two parties. Seehofer leads conservative Catholic Bavaria, opposes Merkel’s mass immigration and her silent downgrading of Israel to embrace Turkey and normalize relations with Iran. Weighing on the AfD, violent nationalistic elements have expressed support for it, providing the press the food for its narrative. Frauke Petry also bears her share of the blame for having waited to distance herself from the Pegida movement.

Lessons from the 1930’s: Although Germany avoids simultaneous state elections in order to keep any one party to come to power too rapidly, experts are dreading next year’s General Federal Elections for the Bundestag (Parliament). One thing will keep the AfD in check though, German companies have been raising salaries by 3-5% every year, thus sharing their growing profits with their employees. Germany has been unique in the West for this sharing of the Economic Rent with workers and retirees. It should help many voters stay in the center and could cap the AfD to 20%.

On Dec. 4th Austria will elect a new President, and I expect the anti-immigration FPÖ to win. Mainstream media is not talking about this, but I see a growing support for one another among Austria’s FPÖ, and Germany’s CSU & AfD. Not to speak of the largest Swiss party, the Swiss People’s Party. As German-speaking Europe shifts against the EU, events in Germany could impact Switzerland. Should the AfD win 10% to 20% of the votes next year, it would be an “earthquake”. Should it surpass the 20% mark, it would bring down Merkel’s rule and end Germany’s enviable post-war political stability.

It is noteworthy, that the Green Party has become the only party in the Bundestag warning of Merkel’s surrender to autocratic & expansionistic Islamic states, as they are perceived in Germany: i.e. her desire to welcome Turkey into Schengen despite the human rights & press freedom record of Ankara, and to normalize relations with Iran while it upholds multiple threats to annihilate Israel. Thus, the CDU is breaching some of Germany’s most sacred Foreign Policy credos since WW2. Merkel’s embrace of the Iranian leader next month in Berlin may only accentuate the silent unease millions of Germans feel about their country embracing and bowing to the demands of somewhat authoritarian Islamic rulers, just as Radical Islamic terror has finally arrived to Germany. This unease is not felt exclusively by skinheads and racist extremists as Berlin and German media portray it. Banking still on Germans’ war guilt & trauma, well meant but excessive efforts by German media to cover up crimes by Islamic refugees and to flood broadcasts with multi-cultural narratives are backfiring. But while the Greens do the ungrateful work, the AfD may harvest the votes.

Turkey and its relationship to Germany is becoming “again” a key factor for German politics. This relationship has a long history that led the Ottoman Empire to enter World War I on the side of Germany and Austria. One event is to many Turks and Muslims as painful as the fall of the Great Caliphate in 1923, that is the loss of Jerusalem after 673 years of Muslim occupation to the British Expeditionary Forces on 11 December 1917 led by General Edmund Allenby after bitter resistance on the Judean Hills and overall 43’000 casualties.

German experts are silent about the fact that Germany is home to approximately 2 millions Turks and 1 million Kurds. Meanwhile, the conflict between the Turkish Army and Kurdish forces is escalating and many Germans perceive Merkel as bowing down to Erdogan in order to fix her strategic error of inviting refugees to Germany and restraining police from properly registering them early on. Watch the CSU closely, it holds the key for AfD’s move into Berlin.

The West is trapped in its constrained perspective of the Orient: As we’ve said before, the West’s lack of understanding of Oriental cultures is proving disastrous for Europe. European leaders use their Roman-Greek linear-logical “glasses” to assess rising Oriental Powers such as China, India, Turkey or Iran. Oriental leaders know that Western leaders don’t understand their Oriental circular-historic way of seeing life and how the Lunar Calendar drives their agenda. Aware of Westerners’ need for written “Treaties”, they use them to advance their geostrategic interests and agenda.

Aware of the circular approach by Turkish geostrategists, we observe since 2002 how Turkey is mobilizing to meet historically painful anniversaries as a Geopolitical Islamic Power: The confluence of history, religion and lunar calendar point to power projection towards Israel, the Sunni Arab World and Germany.

Aware of the circular approach by Turkish geostrategists, we observe since 2002 how Turkey is mobilizing to meet historically painful anniversaries as a Geopolitical Islamic Power: The confluence of history, religion and lunar calendar point to power projection towards Israel, the Sunni Arab World and Germany.

-

In 2017 Turkey celebrates the 500th anniversary of the capture of Jerusalem by the Ottoman Empire

-

In 2017 Britain celebrates the 100th anniversary of the rescue of Jerusalem after defeating Ottoman and German armies. The Christian World celebrates the return of Jerusalem to Judeo-Christian hands

-

In 2023 Turkey marks the 100th anniversary of the fall of the Ottoman Empire, the last Caliphate.

III. The U.S. Elections could change the course of the World Economy and accelerate the current war course

.. along Brexit, a symptom of a much deeper phenomenon that will outlive a Trump administration

We arrive at our 3rd focal point: U.S. Presidential Elections 2016. Many experts say they could be as crucial and direction-giving, as the 1980 elections that Ronal Reagan swept. I personally believe that in 2016 even more is at stake than in 1980. If Clinton wins, markets will rally, assuming business as usual, but they overlook a drift towards some key positions of Trump. Clinton knows how to imitate her opponent’s popular ideas to win. She has a formidable advantage: most media channels and senior journalists are supporting her campaign and shaping what people read and watch. Most importantly, Clinton would shift the Supreme Court to the left-liberal camp and change America for decades to come. But markets are heavily underestimating the geopolitical risks of a continuation of the Obama-Clinton Foreign Policies: According to our latest research, a Clinton Administration is very likely to lead the world to several catastrophic large-scale wars. The Obama-Clinton policies of Forced Regime Change in Syria, Ukraine, Libya etc. along their US-Iran Deal have set the Middle East on course for two wars already.

Should Trump win, I expect world markets to be jolted. He would give the USA a new geopolitical and economic direction; aiming also at distributing the Economic Rent more evenly with more domestic jobs and universal child care. That would come at the expense of Corporate Profit Margins, Global Trade flows and initially also real GDP. Contrary to consensus, our current analysis points to a main scenario with a lesser likelihood of a large-scale war under a Trump administration.

A Trump Administration would have common ground with the May Administration in Britain on the economy, immigration and the need for a stronger military.

The biggest mistake Consensus is making is to project a binary outcome. That is wrong for two reasons: 1st) Clinton is embracing some of Trump’s popular policies to win over his supporters. In less than a year, she has morphed from a Liberal Trade supporter to an anti-Trade activist. Thus, the days of ultra liberal World Trade are counted; 2nd) The USA has 5 to 7 major centers of power, and resistance to the current Policy Mix and NATO is growing. Thus, even if Clinton wins, she won’t be able to overlook the many dissenting forces. Take Obama’s dread for Netanyahu and Israel’s downgrade by the State Department. Yesterday, after strong pressure by the US Congress and the Defense complex (which needs Israeli technologies), both worried about Israel’s security, the USA awarded Israel USD 38 Bn in military aid. Surely, not Obama’s best day.

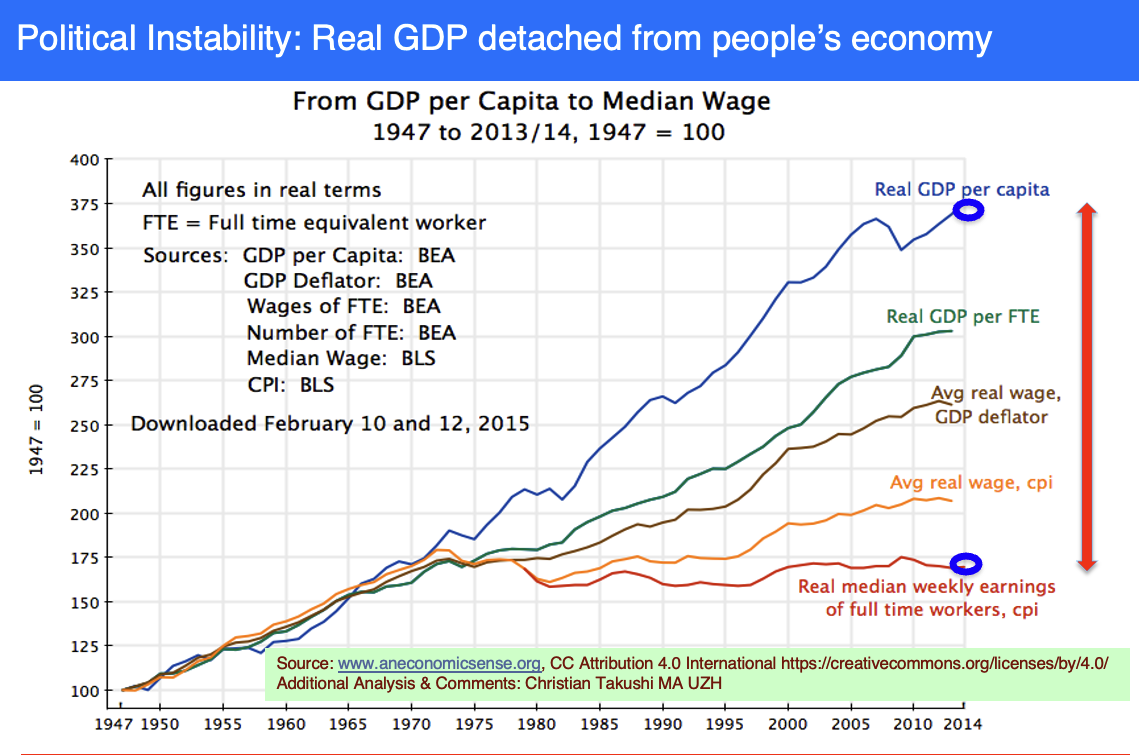

Consensus is paying too much attention to the standard bearers (Clinton and Trump) and not to the forces behind. Since the mid 1970’s real GDP has shot up along Corporate Profits and Trade, but average real incomes for 90% of US workers have stagnated (see attached chart by aneconomicsense.org). Regardless who wins, she or he has to deal with this massive gap that is feeding discontent about the fast-paced concentration of powers in business and politics.

A growing international socio-economic phenomenon has allowed BREXIT to succeed and Trump to win the GOP nomination: Four decades of an extreme Policy Mix are running their course and hitting two walls: GDP, trade and profits are no longer growing organically, and a growing number of citizens no longer accept their stagnating salaries, dwindling job security and level of immigration. In other words, they want their Economic Rent back from Big Firms & shareholders (Capital). Media and consensus focus on how the rise of national sentiment is threatening Globalisation, but underestimate the simultaneous threats to the 4-decade old Policies that enabled it. The Macro Policy Mix comprised Mass Immigration, Liberal Free Trade, Wage Competitiveness (stagnation) and Paper Money Stimulus (printing).

None of these Policies by itself is the problem, rather their convergence at aggregate levels. As Mass Migration and Free Trade are curbed simultaneously for the first time in decades, the impact could be big. Not all G7 nations applied the Policy Mix equally though: Japan decided to skip Mass Migration, and Germany decided to continue sharing the Economic Rent with workers and retirees. That is why Germany has been the most politically stable major economy in recent decades. Until 2015, when Merkel welcomed refugees on humanitarian reasons.

Our research suggests the biggest difference between a Clinton and a Trump Administration shall be felt in the Military Complex: NATO, military spending, new focus and technology. The 1 Trillion Dollar Joint Strike Fighter Program could be an example. Kicked off 15 years ago, it is a major technological leap, but it is mired with significant problems.

Conservative experts blame it all squarely on Obama’s spending cuts, but we should give the President the benefit of the doubt. Our research points to the impact of oligopolistic M&A on technological innovation; oligopolies stifle it. Military Technological Innovation simply didn’t keep up with the expectations set up 10-15 years ago. Obama’s spending cuts only magnified the issues. Big military strategic projects take a decade and imply assumptions about future developments.

Analysts often love to talk about the impact of technology on the economy & investments. They omit the opposite causality direction. Initially M&A had positive effects on bundling research, but in recent years the size of M&A was driven by zero-interest rates. Despite some breakthroughs, the “innovation curve” could flatten further just at a time when military technology should compensate for limited financial resources. This will force Clinton or Trump to seek full access to Israel’s ultra-dynamic Military Innovation, increase military spending and consider to break up gigantic oligopolies.

Following Obama’s spending cuts, the US Military is in retreat mode already, even in Asia. Despite multiple threats, only 2 out of 10 Aircraft Carrier Groups are out containing them. Just as over 14 global geopolitical macro trends converge during 2015-2018, disastrous Regime Change efforts by NATO have been followed by appeasement and apologetic Foreign Policies to all rivals except ISIS and North Korea. Thus, a highly vulnerable world in transition faces multiple risks with no strong US leadership. So, any Risk Event (natural disaster, martial law, election postponement. North Korean attack etc.) during Q4 could quickly unleash a contraction in aggregate demand and trigger a severe market correction. That correction could be an opportunity for an overdue reduction of excesses – if policy makers resist to fight the contraction. Thanks to the FED & ECB, markets didn’t have to price in geopolitical risks since 2008.

In 2016, it is not about who becomes US President, it is about the US Supreme Court: Whether Trump or Clinton wins, the US President doesn’t have the last word in the USA. It can be effectively vetoed. Much more important than Trump or Clinton is the US Supreme Court. These elections are about the shape of the Supreme Court for the next 20 to 30 years. Those judges are there for life; that is why Democrats and Republicans are eager or rather desperate to win these elections. Many judges will have to be replaced soon. Clinton wants to shift the Supreme Court into a liberal camp, while the Republicans want to preserve the long tradition of a Conservative Supreme Courts. Nov 8th may alter the course of U.S. History like now other event since Pearl Harbour. It will be more important than the sweeping victory of Ronald Reagan during the Cold War. So much is at stake, political leaders, banks, business leaders, academia, media and TV channels are all involved in the greatest propaganda war since World War Two. We don’t know who will win yet, but we know already the name of the biggest casualty: the truth.

Christian Takushi MA UZH, 17 September 2016, Switzerland (adapted, released to public on 19 Oct 2016)

General Disclaimer: Global Macro and Geopolitical Analysis are highly complex and subject to sudden changes. No analytical method is without certain disadvantages. We may change our 3-pronged outlook within less than 3-6 hours following an event or data release. Global macro analysis can be extremely time-sensitive and the first 24 hours after an event are critical for the response of a government, corporation, pension or portfolio. Only qualified investors should make use of macro reports and treat them as an additional independent perspective. Every investor should weigh different perspectives as well as “opportunities & risks” before making any investment decision. Not all our reports, research and intelligence is published here. What we release here is delayed and adapted. The research & views we post here for public access are aimed at fostering research exchange (to improve our assessment) and helping decision makers adapt their long term & strategic planning to changing realities, not for short term decisions. If you are not a qualified or professional investor, you should get professional advice before taking any investment decisions.