By Christian Takushi, Macro Economist & Geopolitical Strategist. 3 June 2021 (delayed public release on 4 June 2021 – truncated)

Dear reader

I am convinced that global investors and businesses are still underestimating the rise of Revolutionary Socialism across Latin America. I am warning about it since 2015. The continent is at a crossroads – and Peru elections might well be the tipping point. Not just for the political future of the region, but inflation expectations in financial markets.

I am convinced that global investors and businesses are still underestimating the rise of Revolutionary Socialism across Latin America. I am warning about it since 2015. The continent is at a crossroads – and Peru elections might well be the tipping point. Not just for the political future of the region, but inflation expectations in financial markets.

Many political analysts say this is nothing new: Argentina, Bolivia and Venezuela have been steering left for decades. This widespread belief is flawed and behind many investors’ assessment that the current rise in some commodities is only temporary – i.e. driven mainly by the recovery from the Corona-induced recession of 2020 and Latam politics as usual.

Sadly, the economic analysis and the political analysis on their own (silo-style research) won’t raise any alarms. It is the integrated research of political and economic trends at aggregate levels that sheds light on a few troublesome developments:

Unlike the past 20 years, the current rise of Socialism in the region is an all-out assault on the most capitalistic and successful economies of Latin America: Chile, Colombia and Peru. These three mid-sized economies combined have significant weight. For many years Socialism made noise mainly in dysfunctional countries like Argentina, Bolivia or Venezuela, which are not highly integrated into the world economy. Chile, Colombia and Peru are very different – they are part of the thriving and trade-oriented Pacific Alliance and one way or the other strategic for the USA, the EU, Britain, China and even Russia to some extent.

Peru has been the IMF’s and World Bank’s model economy for the developing world over more than 15 years. Not without a reason: although there is till much social inequality in this Andean nation, 30 years ago its economy was utterly devastated with hyperinflation and poverty rampant. Over 20 years Peru’s free market economic course delivered the probably most stable macroeconomic framework of any developing economy and cut poverty from roughly 58% to 21% in 2019. The Covid-19 Crisis has hit Latin America the hardest – Peru’s poverty rose to 30% over the past 12 months.

But why are the most fiscally disciplined nations of Latin America on the verge to fall to Socialism, Communism or chaos?

Too much Discipline didn’t pay off – Pacific Alliance miscalculated

Peru got the macro economic homework very well, but it failed to modernise its inefficient-corrupt government apparatus and to address social imbalances.

Peru got the macro economic homework very well, but it failed to modernise its inefficient-corrupt government apparatus and to address social imbalances.

Poverty alone would not create the Perfect Storm that these three capitalistic Latin nations are facing. Chile, Peru and Colombia were also too frugal and too strict with their government spending in relation to their neighbours and the rest of world. Can you be too frugal? Yes. If you are fiscally disciplined, but most advanced nations and your neighbours are printing money to finance huge deficits and generous hand outs you will get a social discontent sooner or later – especially if you have extremely active liberal NGO’s stirring your marginalised citizens, and Marxist-Leninist movements agitating them into ever more disruptive and violent behaviour. Most NGO’s mean it well. But many of their workers have morphed into social activists, whose work is being taken advantage of by radical political elements.

At the micro level the persistent underinvestment in infrastructure (health, transport, communications etc.) exacerbated by often corrupted bureaucracy & justice system and the tolerated activity of radical Socialist elements weakened the social cohesion. The stage was set.

Covid 19 was the perfect scenario for the revolutionary left of Latin America. Some liberal thought leaders are only now realising that the work of their most ideology-driven activists laid the ground for radical Socialist movements that are aiming at nationalising natural resources and private property. Officially they promise not to shut down democratic institutions after re-writing the constitution. But knowing their extreme loyalty to the Castro-Chavez ideology of dictatorial revolutionary Socialism, the once thriving model economies of the IMF in Latin America face an existential threat – at the very least the exodus of investors and jobs; at the very worst a repeat of the Venezuelan tragedy.

Geopolitical competition for survival

It is also my view that the model economies of the Pacific Alliance, while being smart macro economically, were sadly somewhat unprepared geopolitically.

If your key neighbours and the leading industrialised nations are printing money to finance their huge deficits, big hand-outs to their citizens, their Covid rescue programs and to prop up financial assets to keep investors looking the other way … while you are still upholding Fiscal Discipline by tightening your belt to finance your way out of a deep Covid recession, you will face a social revolution at home sooner or later. In economics most things are relative – you have to adjust to some extent, especially in an era of instant digital communication, social media and political activism & agitation in your rural areas.

Chile, Colombia and Peru also have tolerated significant foreign activity on their territories and underestimated the plans of their strategic opponents. The Latin illusion that they are all “brothers” blinded them from the fact that the utterly failing huge Mercosur bloc (which comprises Argentina, Brazil etc.) had an existential interest and plans to destabilise their arch rival, the Pacific Alliance. Other nations in the developed world helped their cause, but ultimately, these fiscally brave but geopolitically unprepared nations are responsible for their own trouble, eventually their demise. Brazil played it smart, without any domestic improvement they have dramatically reduced the once huge gap between the ailing protectionist Mercosur and the once extremely open and dynamic Pacific Alliance of Mexico, Chile, Peru and Colombia.

The world has become again a very competitive place; if your neighbour can’t compete with you economically, he will bring you down militarily or politically – the latter being the smarter way.

Castillo Shock in Peru could be much swifter and violent than expected

If the Marxist-Leninist Party wins the presidential elections in Peru, local and regional experts are likely to be overwhelmed by the speed and extent of the market response. I have watched local economists say that the Peruvian Sol would only fall from 3.8 to 4.25 to the Dollar, because the Communist leader Castillo has softened his rhetoric and promised to respect democracy. Well, .. international investors would be naive to follow the advice of local analysts. Their advice is reasonable from a domestic perspective, but not from a global one.

The international investor is risk-averse towards political experiments that depart from established open free markets. With the vaccination process in Developed Markets far more advanced than in Emerging Markets, the risk-reward balance is currently stuck up against Emerging Markets including Peru. If Peru falls, market attention will turn to Chile, where a new market-unfriendly Constitution is currently being written. Chile , Peru and Bolivia could soon be joining forces to nationalise resources. Peru and Chile together are the biggest exporter of copper worldwide. The three are rich in resources. This could drastically reduce investments and production capacity, driving commodity prices higher.

Because both Mr Castillo and the head of his party breathe a radical ideology and loyalty to the Chavez model of revolutionary Venezuela, international investors will be well advised to guard their investors’ interests. They are likely to pull out of Peru as soon as possible. Although Mr. Castillo’s goals might be noble, his country’s high integration into the global economy along its dependence on exports, tourism and global financial markets could unleash a violent economic shock as those sources of income shrink and food prices sky-rocket.

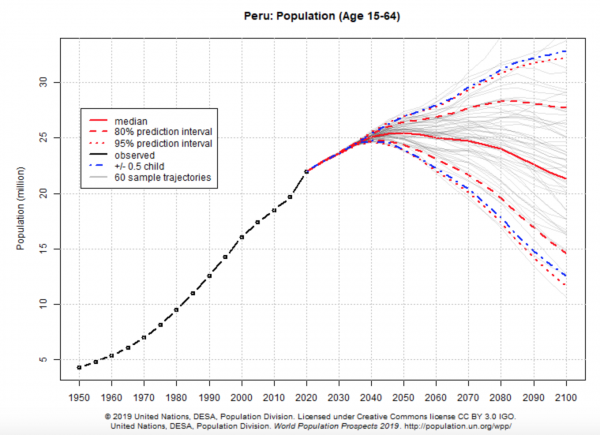

But Peru has something in its favour that few analysts are taking into account – Something that could help generate demand and mitigate the shock. It is still within its demographic sweet spot: The Labor Force is still growing. If access to jobs and food doesn’t collapse, this ‘natural’ source of growth can be a tail wind. Apart from that, Peru’s median age is 30 years old. At that age people are somewhat less inclined to embrace a revolution than at age 20. Most bloody revolutions take place in societies with a very young median age – Venezuelans’ median age was 23 when they embraced Mr. Chavez revolution.

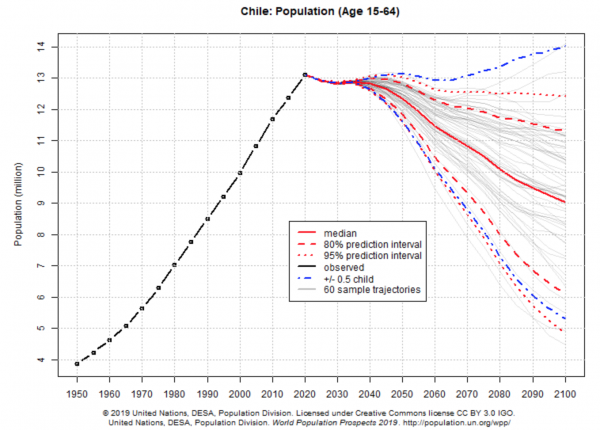

Demographics matters: In Chile the new Constitution will mark an improvement of social rights, but at a terrible cost. The most expected business-unfriendly Constitution will only reinforce the effect of the powerful contraction of the Labor Force that lies ahead, thus resulting most probably in the accelerated decline of the once most prosperous South American nation. Many investors underestimate demographics at their own peril: Once an economy’s labor force peaks due to ageing, real disposable incomes get squeezed and social-political polarisation climbs. It is logical that Chileans would shift further to the left and seek a redistribution of economic rents. Chile’s dire demographic future is not alone – most developed economies (G7) , Russia, Japan, South Korea, Taiwan and China look the same or worse.

Some historians are more optimistic than I am, because they believe the Armed Forced of Peru will intervene in case Mr. Castillo clinches power – just like the military did in Chile after Mr. Allende started to nationalise companies. But after the liberal press and important segments of society treated many military officers that defeated terrorism in Peru as presumed human rights offenders, and terrorists as victims of an internal conflict, it is doubtful many in the military will want to go risk so much again. Interestingly, some analysts think that a new generation took democracy, affordable food and jobs for granted. With countless Peruvians and Chileans saying “we live in a terrible place” and “it can’t get any worse”, it is no wonder millions want a drastic system change. I am afraid they are about to find out, without foreign investments, it is going to get a lot worse for them. The resulting chaos breeding yet more corruption.

Although I will await the results to re-assess the situation on Monday and the race looking highly contested, many analysts see an uphill struggle for the right-wing candidate Ms. Fujimori. If the frontrunner Mr. Castillo wins, I see the Peruvian Sol rising beyond 5 Soles to the Dollar within a few weeks, not years as so many South American economists believe. Why this massive devaluation?

The tragic reality for Peru is this, the global investment community was lied to by Mr. Chavez. He got elected as President of Venezuela promising “No more poor people in a rich country, and the respect of democracy”. But once in power he stack to his radical ideology: you obtain power, never to give it back.

20 years later one of the richest Latin nations is an impoverished dictatorship. All foreign investors that stayed (giving him the benefit of the doubt) felt fooled by Mr. Chavez. Because of the extreme admiration for the Chavez model by Peru’s Communist leaders, foreign investors and business leaders are very unlikely to be fooled this time.

You could say: Investors know how this movie ends. What took investors years to grasp in Venezuela is likely to unfold in less than a year in Peru. This also, because of the brutality of the swing .. this Andean nation would go from being one of the most open, successful and dynamic in the emerging world to being a protectionist Socialist state. From a safe place to invest to a cut-your-risks.

Personally, I will pray that my rather negative predictions in the event of a Castillo win, will not materialise. A miracle is always possible. China may have to “take over” in order to protect her copper supplies. The geopolitical-economic-military balance in the continent could turn decidedly anti-USA. For a seasoned macro economist and strategist, duty and reason come before wishful thinking, so I stick to my very cautious stance and the expectation of an economic implosion should Mr. Castillo prevail.

My personal prediction for the elections’ outcome

Many people have asked me what my personal outlook is. As many of you may know from my past research: I am cautious with polls as most of them work closely with media and are paid by media platforms, which in turn are mostly liberal or progressive (i.e. left). Polls may be statistically very professional, but they live off media outlets. Media is left-leaning all over the world.

Having enjoyed training in statistical analysis, I do my own data analysis in every electoral or economic process I monitor. And almost invariably so far I have detected .. that something is omitted or biased systematically. So far within my research work, in more than 85% of the cases the omissions or biases favoured the left-leaning candidate. Some conservative analysts say these small systematic effects help shape public opinion in the hope to tilt the voting behaviour. Unfortunately, in a geopolitically and ideologically competitive world, many news platforms and pollsters centre their efforts more on influencing public opinion rather than informing the public. Having said that we should not generalise.

As far I am aware no pollster has polled the one million (997’000) eligible voters overseas although they are expected to vote differently from the national average. I also ascertain that most polls have left out people older than 70 years old since voting is no longer compulsory for them. I think there is a hidden vote here for the right wing candidate. Why?

- The citizens overseas tend to be better educated and to earn more compared to the national average. Based on the April 11th voting behaviour and especially given what is at stake on Sunday we could expect these expatriates to vote significantly more right wing than the national average.

- The “older than 70” citizens faced and survived the Leftist military dictatorship and terrorism for 25 years. Many could not cast a vote on April 11th, but now they are vaccinated and probably apprehensive that Communists with some links to terrorism could reach power via elections. Although many of them disliked the former Fujimori regime, they are likely to show up at the polls and vote rather right wing.

This could add 0.5% to 2% to Ms. Keiko Fujimori of Fuerza Popular (party) – maybe just enough to tip the balance in favor of the center-right coalition. Nevertheless, we are dealing here with a highly contested election and there are many reports that violence is being used in far away rural areas by the Communist party.

Copper price shock could trigger a shift in Global Inflation Expectations

Many policy makers are monitoring elections in Peru with elevated levels of concern. They needed markets to accept negative real interest rates – This was working for them pretty well. Their message: Inflation will overshoot temporarily, but don’t worry we got it under control, so we will keep interest rates at record low levels. But if Peru shocks commodity markets, and Chile is seen as following suit, the whole commodity complex including gold could signal higher inflation yet. Over the past two weeks inflation numbers began to overshoot targets. It is against this tense monetary backdrop that these Peru elections are taking place.

Many economists are saying that the current commodity price increase is due mainly to the economic recovery from the Covid-related recession last year. What they overlook is that after 40 years of money printing – of which the last 11 were of an extreme magnitude – the hyperinflation central bankers orchestrated in financial assets (bonds, stocks and real estate) is finally spilling over into commodities. This has happened before in economic history: excessive monetary growth seems to be under control (creating inflation in desirable assets at first), but at one point it spills over into the wider economy.

Against consensus, we have been warning for eleven years that extreme money printing coupled with artificially low interest rates will weaken the world economy and create both, powerful deflationary forces and inflationary forces.

Truncated – If you want to read the full research report, you can subscribe to our newsletter on our landing page.

By Christian Takushi MA UZH, Independent Macro Economist & Geopolitical Strategist. 3 June 2021 (delayed public release on 4 June 2021 – truncated)

Disclaimer: None of our comments should be interpreted or construed as an investment recommendation

A distinct broad approach to geopolitical research

(a) All nations & groups advance their geostrategic interests with all the means at their disposal

(b) A balance between Western linear-logical and Oriental circular-historical-religious thinking is crucial given the rise of Oriental powers

(c) As a geopolitical analyst with an economic mindset Takushi does research with little regard for political ideology and conspiracy theories

(d) Independent time series data aggregation & propriety risk models

(e) Takushi only releases a report when his analysis deviates from Consensus